Why did Software sell off today? | ROKO | Planisware strong updates

Todays software sell off

The overnight sell-off in global software stocks was triggered by news out of Thoma Bravo — the world’s largest software-focused private equity fund, managing approximately $181 billion in assets. Yesterday, the firm finalised one of the largest write-offs in software industry history, crystallising a $5.1 billion equity loss on its 2021 acquisition of Medallia.

The business itself hasn’t collapsed or been disrupted by AI. Medallia’s customer experience platform remains operationally intact and profitable. This was a pure capital structure failure: too much debt, no principal repayment since acquisition, deteriorating software valuations across the market, and ultimately an inability to refinance with its private credit syndicate — which included KKR and Blackstone. When the PIK relief window expired at end of 2025, the lenders refused to extend it, and the keys were handed over.

We view this as rationality returning to the market. A genuine cost of capital is reasserting itself, and over-leveraged buyers are being forced to the sidelines. For long-term holders of Constellation Software, Lumine, and Topicus — companies that have always acquired at disciplined prices with conservative balance sheets — this dynamic is structurally positive.

Röko Q1 2026 — Quarterly Update

Q1 2026 was a solid quarter for Röko. Organic momentum is building, the acquisition pipeline is active, and the business continues to compound in the way it was designed to. Here’s what the numbers show and what management had to say.

The Numbers

Net sales grew 9% to SEK 1,853M, with 6% of that coming from organic growth — a meaningful step up from the 2% organic growth delivered in Q1 2025. The remaining contribution came from acquisitions made over the past year.

Adj. EBITA came in at SEK 415M, up 5% year on year, with the margin compressing slightly from 23% to 22%. That one percentage point of margin dilution is largely a function of timing — three acquisitions closed near the end of the quarter and contributed minimal earnings but added to the cost base. As those businesses are integrated and their earnings normalise into the run rate, margin should return to trend.

The standout line in Q1 was operating cash flow: up 22% to SEK 255M. For a compounder, cash conversion is the scorecard that matters most, and this result is encouraging.

Five Years of Progress

Zooming out, the trajectory since FY2022 is worth appreciating. Net sales have grown from SEK 4.3B to SEK 6.5B. Adj. EBITA margin has expanded from 18% to 21%. ROCE has climbed from 12.7% to 14.8%. And the company count has grown from 22 to 33 — with a head office of just 8 people.

That last point is the most Röko thing about Röko. A HQ of 8 overseeing 33 operating businesses across multiple countries and currencies is not a coincidence — it is a deliberate structural choice that keeps costs out of the centre and accountability close to the customer.

Acquisitions

Three acquisitions were completed during the quarter, all of which closed near period end and therefore made a limited contribution to Q1 earnings. Annualised, the acquired revenue run rate of SEK 552M is the largest in Röko’s history — well ahead of any prior year.

The three new additions are:

Lambda SpA (Italy) — lasers for dentistry and veterinary applications, with global sales. Enterprise value: 11 MEUR.

GolfShopen (Norway) — market-leading golf equipment retailer in Norway. Röko has owned the equivalent Danish business since 2021, so this is a natural geographic extension. Enterprise value: 250 MNOK.

Access Building Products (UK) — market leader in access panels and door canopies. Enterprise value: 15 MGBP.

What Management Said

A few themes that stood out from the Q1 commentary:

On organic growth: Management is actively educating portfolio companies on price discipline. The 6% organic growth in Q1 reflects this work beginning to show up in the numbers.

On deal flow: The pipeline remains healthy, with attractive opportunities across multiple markets. Importantly, management noted a general loosening of deal flow — larger businesses in particular are beginning to come to market. Röko is increasingly recognised as a credible acquirer in several countries, which is improving the quality of inbound opportunities.

On capital discipline: Despite the strong pipeline, management was clear they do not want to over-deploy in any short period. The preference is to invest well rather than invest fast. At the same time, they expressed confidence in the team’s capacity to handle a higher volume of deals as the platform scales.

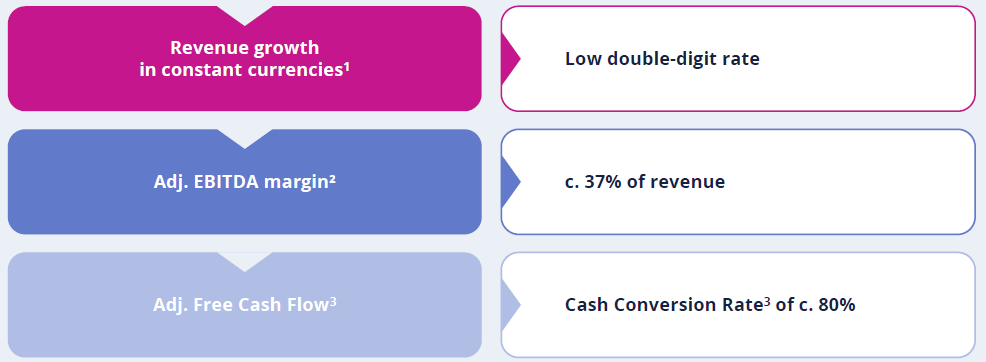

Planisware - Q1 results & Outlook

Planisware released strong sales and trading results for the 1st quarter of 2026 with Q1 revenue +13.6% on prior year and accelerating growth in SaaS and hosting revenues. They also re confirmed their 2026 targets for low double digit revenue growth at 37% EBITDA margins, the stock has recovered slightly but still only trades on 16x Pre-tax earnings.